MSMEs have been badly hit due to COVID19 need additional funding to meet operational liabilities built up, buy raw material and restart business. Gove...

-20191015034423-28-20200306040946-22.svg)

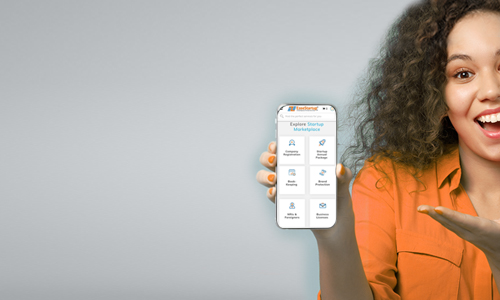

Company Registration, GST Registration, Startup Registration, Trade Mark and much more.

Credit/Debit Card, Net Banking & Wallet options. Flexible EMI without Credit card. Instant Approval.

No need to fill-up a lengthy form. Just click a selfie of your documents and relax.

Focus towards your Startup growth, Get consultation on Branding, Funding and much more.

MSMEs have been badly hit due to COVID19 need additional funding to meet operational liabilities built up, buy raw material and restart business. Gove...

SPICe Plus- New initiative for Ease of Doing Business for Startups...

Consequences of Non-filing of GST return ...

All will be interested to convert their ideas into the business. Business is basically a blueprint that will convert your ideas from the startup phase...

Many startups got confused between Private Limited Company and Limited Liability Partnership. Lets discuss the key features in both....

The first step that is to be done after incorporation of the company is the holding of the Board meeting of the Company. Every Company is required to ...

Ezeestartup.com is owned by Ezee Startup India Pvt. Ltd. Its a group of professionals having diverse knowledge and experience, who have come together to start this venture to provide a wide range of value-added services to startups for their new ventures and for existing clients. The first step of entrepreneurship is to set-up an entity to house your business. Taking this first step is the most difficult one in the start-up journey. We at Ezeestartup help you in every step of setting-up your full start-up ecosystem.

Read More

Are you CA/CS/Lawyer/Management Consultant/Multimedia Experts/Graphic Designer/Content Writer/Digital Marketer/Website Designer/Software Developers/Digital Solutions Provider, Join us and grow your business.

Join Us NowThanks to your team and the assistance from EzeeStartup. It's refreshing to deal with someone who promptly offers solutions and service, I am glad I chose to use your services and I am completely at ease after availing your services.

First EAZIEST step to become an Entrepreneur. The work was above and beyond what I could have expected. Great job!. Excellent hassle free service all the way around from start to finish. Keep it up the GREAT work. Must recommend.

The service and personal attention is extraordinary, reliable in time commitments, and overall consistent in meeting our expectations.

Greetings! Well done Ezee Startup team!!! Ezee Startup company and their whole team is excellent, we preferred and selected Ezee Startup by discard our original Consultant for our Company registration. Their whole team is polite, well professional and moreover experienced and they guided us on each and every stage for our Company approval. They have well written procedures and kits which gives clear guidance on govt procedures for us, this I do not found with any other Consultants. Their staff work full time and supportive. I would Congratulate Ezee Startup team and wish them all the Best for their future. Hire Ezee Startup is peace of mind and value to the money. I strongly recommend for hiring their services.

These guys are just absolutely the best at their work. Humble and professional in their work approach. They have helped me set my company when I knew nothing about all the legalities. Their support team understands the customer well. No need to look elsewhere for legal purposes for start-ups. Kudos to you guys, keep it up.

Certified by

Payment Gateway Partner

Payment Gateway Partner

Payment Gateway Partner

Banking Partner